Here in The Future of Finance, we previously

introduced you to the Evergreen Direct Investing (EDI) architecture, the focus of the fifth case study in our Field Guide to Investing in a Regenerative Economy initiative. The blog posts were: “6 Reasons Stock Markets Are No Longer Fit For Purpose” & “How Stewardship Investors Can Drive the Great Transition to Regenerative Propserity.”In the months since, we and Senior Fellow Tim MacDonald have continued to explore how this investing tool can enable values-aligned enterprises and stewardship investors to co-create the regenerative economy. We share with you here a two-part series about the method authored by John Fullerton forCSRWire’s Talkback blog.

To download the full EDI study, please click here.

Part I – “Evergreen Direct Investing: ESG 2.0”

Despite the monumental progress of the responsible investing movement into the mainstream, proponents of “ESG” on the corporate side and the investor side face one major obstacle: too many investors simply don’t care. And even when institutions care, signing onto The United Nations-supported Principles for Responsible Investment (PRI) for example, changing investment decision-making at the portfolio manager level is slow at best. How come?

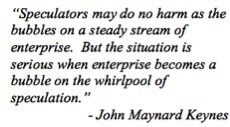

We have lost the distinction between investment and speculation.

Keynes well understood the vital role of speculators in a market system, but also understood the importance of its appropriate scale in proportion to real investment and the primacy of enterprise over capital markets in a healthy economy. We now refer to speculators of all stripes, from George Soros all the way down the food chain to criminal enterprise operator Stevie Cohen, as “investors,” suggesting a more genteel legitimacy. Similarly, JPMorgan has a Chief Investment Office not a Chief Speculator Office. Although if it walks like a duck and talks like a duck…

Less in our conscious awareness, however, is the fact that as a trading culture has taken over our financial markets in the new millennium, even what we think of as “real investors” – the portfolio manager at Fidelity for example – have been sucked into the short-term speculative stock price valuation game, in stark contrast with the real capital investment decisions being made by corporations themselves in the real economy.

CSR, ESG: Does It Make a Difference?

We find ourselves with “CSR” focused largely on supply chain management, while the responsible investment movement using its “ESG” framework is focused largely on speculators (who don’t care really) rather than the real investment decisions being made in the capital budgeting process of corporations themselves. Similarly, the investment budgets of government entities such as the largest single energy user in the world, Uncle Sam, must be the focus of our ESG lens. I recently asked the Chief Financial Officer of a “CSR” leading Fortune 100 company how they factored their social and environmental metrics into their capital investment decisions. He smiled, essentially saying, “those decisions are hurdle rate-driven” (with no imputed price on carbon, for example). That is the real world today.

Rerouting the Capital Investment Process

But imagine a different world. Imagine a world where real, large-scale investors with clear long-term stewardship responsibilities such as pension funds, endowments and sovereign wealth funds take a more direct role in the capital investment process. Rather than eating off the short-term speculator-dominated menu our conflicted, modern Wall Street serves up, imagine stewardship-minded investors negotiating direct relationships with corporate management with an explicit requirement to build long-term ESG values and parameters into the enterprise capital investment process, even if it entailed some short-term negative consequences. And imagine more mature corporations with stable cash flows following the successful example of MLPs and REITs that pay out the vast majority of their cash flows to investors rather than hoarding their capital, requiring them to go back to investors for their capital investment needs.

Contrast the 10- or 20-year investment performance of the MLP and REIT sectors, with that of the S&P 500, or the stock MSFT for that matter. Paying out cash flow to owners disciplines the capital investment process, which translates directly into strong investment performance and rewards long-term investors. Warren Buffett understands this.

Leading a Sustainable Economy—For the Long-term

Now imagine merging the imperative of integrating ESG values and objectives responsible investors have signed up for in the PRI, with a direct enterprise investment method centered on long-term private partnerships among stewardship investors and enterprise leaders that truly want to lead the transition to a sustainable economy.

At Capital Institute, we call this Regenerative Investment and the method is called Evergreen Direct Investing (EDI), conceived by our Senior Fellow Tim MacDonald, leveraging his practical experience in the world of private real estatepartnerships. The latest case study in our Field Guide to Investing in a Regenerative Economyinitiative describes the EDI method in more detail. Importantly, it describes how investors can earn acceptable and resilient returns by investing directly in the stable cash flows of mature, slow- or no-growth business enterprises that the valuations-game-driven speculators leave on the trash heap. Does EDI hold out the promise of ushering in “ESG 2.0” and the prospect of a resilient but low growth developed world economy that is our reality in the face of planetary boundaries? We think the answer is an emphatic, “yes!”

In part two of this column, we will look at Evergreen Direct Investing from the perspective of enterprise leaders.

Part II – “Evergreen Direct Investing: The CEO Perspective”

In Part 1 of this series on Evergreen Direct Investing (“EDI”), we argued that the Responsible Investment movement seeking to embed ESG values into investment decision-making has been hamstrung by the investment method chosen. Specifically, trying to apply ESG to what is inherently a speculative stock valuations game often feels like pushing on a string. Without conscious awareness, we have confused speculation for investment.

We suggest that by shifting investment capital away from the speculation game around which modern portfolio theory (with its many limitations) was designed and into what we are calling the Evergreen Direct Investing method (conceived by Capital Institute’s Senior Fellow Tim MacDonald), stewardship-minded investors, such as pension funds and endowments, can achieve attractive and resilient long-term financial returns that match their liabilities, while directly embedding ESG values into negotiated investment partnerships.

Here in Part 2 we will look at the Evergreen Direct Investing method from the perspective of the CEO. If EDI is to scale up to complement the public-market, business-as-usualalternative – and to have a meaningful impact on the sustainability challenge facing, in particular, the large, mature businesses operating in the low growth developed economies – it must be appealing to both investors and enterprise leaders. EDI passes this test with flying colors for management teams that possess the long-term horizon that a transition to a sustainable economy demands.

EDI Must Appeal to Business Leaders

The core architecture of EDI is the cash flow sharing method that already exists in numerous private real estate investment partnerships. Typically, investors get priority access to cash flows until they get their investment returned, and then some preferred return of, say, eight percent. Beyond that, profits are split between the investors and the sponsors.

We envision EDI being applied to the mature, stable cash flow businesses that are often the “cash cows” of public companies. These low- or no-growth cash flow generators are often derided by investors, seen as obstacles to getting the stock price higher in the growth dependent, speculative valuations market (otherwise known as the stock market). New growth opportunities need to be very large in order to “move the needle” relative to the large (but often no longer growing) core business. Think of Microsoft’s challenge of creating enterprise growth in relation to the mature but low-growth domestic Windows and Office business lines. Microsoft stunningly has largely failed to generate returns for public investors for over 15 years until the market got wind of the looming management change.

Now imagine a group of pension investors partnering to invest directly into such a mature, low-growth business with the resilient cash flows needed to match their liability streams. An EDI partnership could be constructed in which the investors acquired, say, a 40 percent stake directly in the mature business cash flows. They would receive 100 percent of the cash flows attributable to their share (after necessary maintenance capital expenditure) until they received their investment back. These investors would then get, say, 80 percent of the cash flows until they earned a preferred return ofeight percent (IRR). After that, the cash flow split would reverse, with investors getting 20 percent of the remainder (forever) while 80 percent reverts to the enterprise (including incentive compensation for management).

Facilitating True Alignment of Interests

Rather than management being compensated with stock options giving them an incentive to pump up the stock price in the relative short-term, now management has the incentive to manage this mature business for the long-term.

The sooner management can satisfy the investor’s preferred return, the sooner management and employees get to enjoy the lion’s share of the subsequent cash flows. They can decide to reinvest at that time, or, if suitably attractive investment opportunities are lacking, pay out that cash flow to employees and themselves as negotiated in advance with the investors. Investors could, of course, stipulate numerous other stakeholder-friendly uses of this “free cash flow,” limited only by their creativity.

In this way, incentives are truly aligned with investors, de-risking the investment in the process, thereby lowering the appropriate cost of capital. By embedding ESG values and objectives in the partnership structure, all stakeholder interests can be negotiated upfront with unlimited innovations. Even financial advisor compensation can come out of future equity splits (in whole or in part), thereby truly aligning the interests of financial intermediaries for the first time.

How long is the long-term view required by EDI management teams? Keep in mind that EDI will typically be applied to stable but low- or no-growth businesses. Such businesses are valued in the speculative valuations market quite low, say, five to six times cash flow. Even after allowing for necessary maintenance capital expenditure, such businesses should generate a cash on cash return in the low- to mid-double digits, enabling a return of capital to occur in seven or eight years. In such a situation, management teams need at least a 10-year view and commitment. Such a timeframe is appropriate, and means the transition to sustainable, and in fact regenerative, business models is actually feasible.

Living Proof the EDI Method Works

One need not look past one of America’s “most admired CEOs” Rich Kinder, founder of Kinder Morgan (“KMI”), to see an example of a leader utilizing an Evergreen-Direct- Investing-like vehicle – in this case publicly-traded Master Limited Partnerships that pay out virtually all their cash flow to investors and then go back to investors when expansion capital projects require additional capital. Rich Kinder recognized the value of the dull, boring “asset heavy” pipeline business inside Enron that public shareholders wanted no part of, while Jeff Skilling was working his magic with derivatives. Rich Kinder, now a billionaire who draws a dollar a year salary, is living proof of the value creation potential of thereal investment approach of EDI, for investors, management and employees.

What remains to be done is to align the power of the EDI approach with the sustainability challenges ahead. Rather than apply this method to yesterday’s fossil-fuel-based energy infrastructure as Rich Kinder did nearly 17 years ago, next generation enlightened CEOs will leverage the power of the EDI method to create the regenerative enterprises of the future. These CEOs will lead the transition to a sustainable economy while delivering resilient value to investors and all stakeholders by embedding transformative ESG values into future direct investment partnerships.

We call this “ESG 2.0.” Let’s get started.